Can you get a credit card with no credit checks? Yes, it’s actually possible with the neo-banks credit cards to rebuild credits.

Credit cards offer a credit line for a borrower. It is a debt product that helps a borrower use a credit facility from the issuing bank. Credit cards do a credit check for the borrower before issuing a credit card. If you have fair or bad credit, getting a hard credit check might further affect your credit. You can opt for credit cards with no credit checks.

These credit cards do not put a hard inquiry on your credit score. Instead of relying on the traditional credit score such as FICO, they rely on the financial history of a borrower. They use proprietary algorithms to assess the creditworthiness of card members. They then issue a credit card with a limit for the user. Like any other credit card, paying on time can help build long-term financial health as well as traditional credit history.

Use cases for credit cards with no credit checks

These credit cards are best suited for people with no credit history or fair credit history. People with bad credit history may find it difficult to rebuild their credit. Instead of relying on touts or credit-building companies, they can either apply for secured credit cards. Another, option available is to use these credit cards which do not affect the credit score.

These credit cards are issued by neo-banks or new-age banks. Unlike traditional banks, which rely on FICO scores or credit scores from credit bureaus. These neo-banks build sophisticated algorithms to determine credit worthiness of members. They rely on your banking transactions, payment histories, and other financial histories to define your credit line.

Best examples of credit cards with no credit checks

Let’s now dive into some of the credit cards available in the market today, which require no credit checks.

TomoCredit Worldelite Mastercard

TomoCredit Worldlite Mastercard

Fees: None

APR: None

Rewards: Tomo doesn’t offer any rewards to users for now.

In a nutshell: TomoCredit does not rely on the credit score to calculate the creditworthiness of a member. They ascertain the same based on their unique algorithm.

The spending limit on this credit card varies from $100 – $10,000. A user has to be pre-approved before they can get this credit card. If you are declined, you can’t reapply for Tomo credit card.

TomoCredit helps improve the credit score of card members. Additionally, they report to all three major US credit bureaus.

As this card has no requirement for a credit score, it is great to build the same. This is a great card for people with poor credit scores.

Tomo requires you to connect your banking account with their system. Once, they run their algorithm on your financial history to assign you a credit limit.

Members have to make a full payment of their dues at a pre-determined payment cycle. This payment cycle can be weekly, bi-weekly, or monthly. If you don’t pay your bills on time Tomo doesn’t charge you any interest but freezes your account.

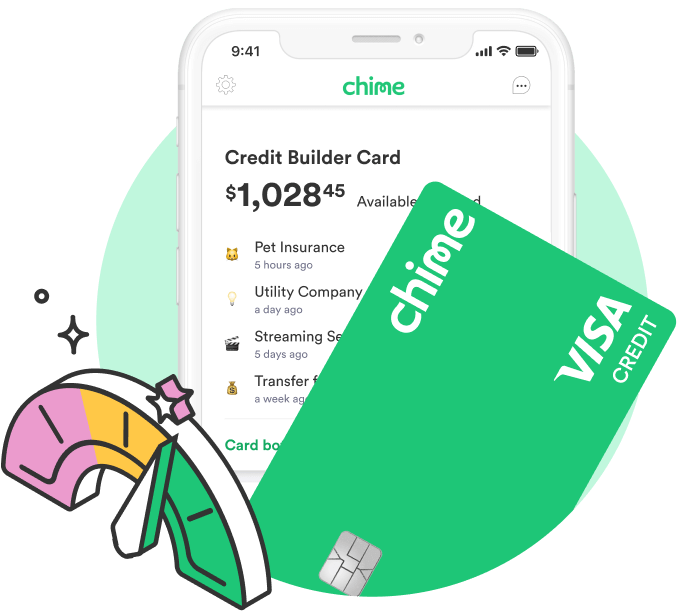

Chime Credit Builder Secured Credit Card

Chime Credit Builder Secured Visa Credit Card

Fees: None

APR: None

Rewards: Chime credit builder visa credit card doesn’t offer any rewards for the users.

In a nutshell: The Chime Credit builder secured credit card is a Visa credit card issued by Stride Bank. Further, this credit card has no annual fee or interest rate.

Additionally, the chime credit card has no minimum requirement for a security deposit. Though, the best feature of this credit card is that it doesn’t require a credit check to apply for it.

Although, for qualifying for this credit card you require a Chime credit builder account. Cardmembers can deposit their funds directly to their Chime credit builder account. Against this direct deposit, they can use their credit card to make everyday purchases.

Further, members can pay their dues by using the money in the credit builder account. Building good credit habits and on-time payments will help users build their credit scores over time. Chime credit builder could also be a good financial product for a beginner as well. Even non-USA citizens can apply for this credit card. This could also help them build their credit score in the USA.

OpenSky Secured Visa Credit Card

OpenSky Secured Visa Credit Card

Fees: OpenSky Secured Visa credit card charges a low $35 annual fee to card members.

APR: None

Security Deposit: Low-security deposit starting from $200 and can go up to $3,000.

Rewards:

In a nutshell:OpenSky Secured Visa credit card is a secured credit card. This credit card starts as a secured credit card. But, a user can improve their credit score through good financial habits. Once, they improve their credit score they can upgrade to an unsecured card in 6 months. OpenSky reports to all 3 major credit bureaus in the USA.

Cardmembers can start with a low-security deposit of $200 and a maximum of up to $3,000. Once they deposit this security amount, their credit card is approved for usage.

Members can use the credit card to make normal everyday purchases. In order to, provide a boost to their credit scores, they should try and keep their credit utilization under 30%. Further, they can start paying their payments in full or at least minimum dues to help rebuild credit.

No one likes to pay the annual fees of a credit card. People try their best to get away with not paying credit card fees. $0 annual fees credit cards offer some of the best rewards to the user with the perk of no annual fee.

Our list of some of the best credit cards with $0 annual fees

Best Rewards Credit Card – Chase Freedom Flex Credit Card

Chase Freedom Flex

Fees: Chase Freedom Flex credit cards charge $0 in joining and annual fees

Intro Rewards: This credit card offers a $200 bonus on a spend of $500 in the first three months of the card approval. It also offers a 0% introductory APR for 15 months on balance transfers and purchases.

Rewards: Freedom Flex offers 5% cash back on purchases from grocery stores, gas stations, and select online merchants. Further, it also offers 5% cash back on travel purchased through Chase Ultimate Rewards.

In a nutshell: Chase Freedom Flex Card offers excellent rewards on everyday purchases categories. For example, groceries, gas, and online merchants. Though, it also offers 5% cash back on travel through Chase Ultimate Rewards. This card also offers a 3% cash back on dining at restaurants and drugstore purchases. For all the other purchases, there is a cashback of 1%.

Cash back never expires on this card. This card also offers Zero Liability protection and purchase protection. Further, other additional offers and benefits are available from Mastercard.

Travel Rewards from Bank of America

Bank of America Travel Card

Fees: $0 in Annual fees, a 3% fee on the balance transfer, and $0 foreign transaction fees

APR: 0% APR offers for 18 months

Rewards: Customers can earn 25,000 bonus points and a $250 travel or dining statement credit value. In order to, qualify for this offer they have to spend at least $1,000 in the first 3 months of opening the new card account.

In a nutshell: This credit card also offers excellent travel rewards with 3 points earned for every $2 spent on purchases. Customers get the flexibility to redeem points for a statement credit. They can also pay for travel and dining purchases made on the card through rewards. Further, there are no end dates of the points expiry on this card and there are no blackout dates.

Additionally, existing Bank of America customers receive higher bonus rewards. Bonus rewards depend on their Preferred Rewards tier with the Bank. For example, a preferred customer gets more points.

Best Credit Card for People with Fair Credit – CapitalOne Platinum Mastercard

CapitalOne Mastercard

Fees: This credit card is available with $0 in annual fees. It also offers $0 foreign transaction fees.

Joining Rewards: This credit card doesn’t offer any joining rewards.

Rewards: Mastercard offers $0 Fraud Liability if the card is either lost or stolen. Capital One has a tool to monitor the credit profile of a user. Card members get unlimited access to their credit score CreditWise from Capital One.

In a Nutshell: This is one of the best credit cards for members with Fair credit. This card automatically increases the credit limit of the user over time. They can consider increasing the credit limit starting in as little as 6 months.

CapitalOne takes into account payment history patterns to raise the limit. Finally, this is a great credit card for a starter person looking to build credit.

Capital One SavorOne Rewards for Students

CapitalOne SavorOne Student Rewards

Fees: This credit card charges no annual fee and no foreign transaction fee to their users.

Rewards: Card membersearn unlimited 3% cash back on multiple categories. For example, the rewards are for dining, entertainment, popular streaming services, and at grocery stores. One-time $50 bonus on spend of $100 in first 3 months of card opening.

In a nutshell: Students from universities, community colleges, or other higher education institutions can apply for this card. This card helps students build their card history over time. Students receive a complimentary Uber One membership and 10% off on Uber and UberEats orders. They also receive unlimited 5% cash back on hotels and rental cars booked through Capital One Travel.

Best Secured Credit Card – DiscoverIt Secured Credit Card

DiscoverIt Secured Credit Card

Annual Fees: $0

Minimum Security: $200

In a nutshell: DiscoverIt Secured credit card requires a minimum $200 refundable deposit and offers the credit lines equivalent to the deposit. This card provides 2% cashback on fuel and restaurant and 1% cashback on other purchases. Discover also offers unlimited cashback matches for the first year.

Meanwhile, if a customer has a good payment history of six months, they release the deposit. This credit card also reports to the three major bureaus and helps build a credit score. This card offers one of the fastest six months upgrades to an unsecured credit card. Customers have to ensure a timely payment across their credit cards and on-time payment history.

Citi Simplicity Credit Card

Citi Simplicity Credit Card

Introduction Balance Transfer APR: 0% Intro APR for 21 months for balance transfers. Additionally, 0% intro APR for all new purchases for the first 12 months.

Regular APR after the Introductory period: Once the introductory period is over, a variable APR of 18.49% – 29.24% is charged. This APR will be on the creditworthiness of the customer.

Rewards: Citi Simplicity credit cards do not offer any rewards. This credit card is not meant to be a rewards credit card.

Fee: Citi simplicity credit card doesn’t charge any annual fees, late fees, or penalty fees.

Other Fees: Intro fees of 3% of balance transfer fees (least of $5) for the first 4 months of credit card account opening. After the Intro period, 5% of balance transfer fees (subject to $5). 3% of foreign transaction fees are applicable on foreign transactions.

Pros and Cons of this card: Citi Simplicity credit card is one of the best 0% APR credit cards. As this credit card offers a 0% introductory offer for all new purchases for 12 months. Customers can also use it for making big purchases. They can then pay the amount over a year.

Though this credit card does not offer any rewards, it offers the best balance transfer period of 21 months. Additionally, it offers 12 months of 0% introductory offer on new purchases.

Best Credit Card for Rent Payment – Bilt Mastercard Credit Card

BILT Mastercard

Fees: This credit card charges $0 in Annual fees and foreign currency conversion fees

APR: 20.24% – 28.24% of variable APR

Rewards: BILT MasterCard lets the cardmembers earn points on paying rent. This card provides a 1% reward for paying the rent. This credit card does not charge any transaction fees. There is a limit to the total 50,000 points which members can earn from rent.

Pros of this Card: Bilt Mastercard offers 2x points on travel purchases.Card members earn points on flights, hotels, rental cars, and cruises. In order to qualify, the travel is to be booked directly with airlines, hotels, and car rental agencies.

The card also offers the members 3x points on dining. On the rest of the purchases, the card offers 1 point. All the expenses on the 1st day of every month offer double the rewards. Members get 6x points on dining, 4x on travel, and 2x on other purchases. Further, rent payments on the 1st do not qualify for this offer.

Bilt has been ranked as one of the most valuable reward points by Bankrate. It has been ranked above American Express cards and Chase Rewards cards.

Bilt offers up to $5,000 reimbursement for a non-refundable passenger fare. If for any covered reason the trip is interrupted or canceled. Bilt also offers reimbursement for expenses incurred on delayed trips over 6 hours. Covered reasons include Weather, aircraft breakdown, or air traffic control delays. In order to, qualify for this offer the card members need to book the entire trip on the Bilt Mastercard.

This card also offers Auto Rental Collision Damage waiver for any rental car charged on the card. BILT MasterCard offers better points as a rent or travel card.

Business Advantage Customized Cash Rewards credit card

Business Advantage Customized Cash Rewards

Fees: This credit card charges $0 annual fees.

APR: Introductory 0% on purchases for the first 9 billing cycles. Once, the intro APR offer ends a Variable APR that’s currently 15.99% to 25.99% will apply.

Rewards: Card members earn a $300 statement credit after they make at least $3,000 in purchases in the first 90 days of the account opening.

Pros and Cons of this card: Firstly, credit card members earn 3% cash back in the category of their choice. For instance, gas stations, office supply stores, travel, TV/telecom & wireless, computer services, or business consulting services. Next, this card offers 2% cash back on dining purchases.

Card members earn unlimited 1% cash back on all other purchases. Customers can also earn up to 75% more cash back on every purchase. But to qualify they need to have a business checking account with Bank of America. They need to also qualify for the highest Preferred Rewards for Business tier for the best rewards available.

We all face a dilemma sometimes when our credit card declined in the middle of a transaction. This could be an embarrassing situation if you are using your credit card to purchase a service. Imagine having a great lunch at a restaurant and putting in your credit card for payment. The server informing that your credit card declined to pay.

A credit card may decline due to a number of reasons. In order to, avoid the heartache of handing over a credit card and facing a declined card, we recommend checking a few things beforehand. It’s always good to enable notifications from credit card providers. Also, enable the notification service from your mobile or cell phone to get a notification alert.

Credit cards may decline to pay in case of using an expired card, foreign transactions, large payments, and some cases incorrect data input.

Balance exhausted or Credit limit reached

The most common reason for a credit card to decline is overspending or shooting the credit limit. Every credit card comes with a credit limit, which is pre-set by the bank. Further, this credit limit defines how much a user can shop or use the card for a purchase. If a user hits the limit on his credit card. Consequently, if they try to purchase or use a credit card beyond this limit, the transaction will fail.

Do not spend too much money or have a large outstanding balance on the credit card. Always, keep your balance under the defined credit limit. If you need help managing credit card debt, do read our best tips to manage credit card debt.

Sometimes, you might have put an automatic payment like a utility bill or tax payment on your credit card. If that transaction hits your credit card, it may take 2-3 days to appear in the credit card summary. The credit limit immediately reduces to factor in the impending transaction. Further, if you hit the limit of the card and try to make any transaction the same may be declined.

Otherwise, if you have made a payment on a credit card to restore your balance, give at least 2-3 business days for the amount to settle in the credit card. Don’t expect that the balance will be immediately restored. Consequently, the balance of a credit card is increased only after making a payment.

The Credit card is expired leading to the card declined

Every credit card comes with an expiry date on the front of the card. Sometimes we might miss that a credit card has expired and may try to use it. An expired credit card will be declined.

Additionally, banks and credit card companies cancel expired cards. As the same is no longer valid in their systems, holding an expired credit card is like holding a piece of plastic.

Swiping the credit card

Using credit cards outside the USA

New credit cards disable the option of foreign transactions by default. Before you can use a credit card for a foreign transaction, you have to enable the same. You can enable foreign transactions from the website or the mobile app of the bank. Alternatively, you can reach them over call to enable the same.

Secured credit cards or basic credit cards are not available for foreign transactions. These cards do not allow foreign transactions at all.

Card declined on making an unusually large purchase

Credit cards may decline a usually large purchase on your credit card. They may suspect a large sum on your credit card is a fraud or theft transaction and may decline the same.

Say you have a credit card with a $5,000 limit. Usually, you make small transactions (under $500) with this credit card. You did a large purchase of day $4,000 on your credit card. This unusually large transaction may flag off risk systems. The bank may decline this transaction.

The Credit card is not in use for a long time

If you are not a frequent credit card user or if you have multiple cards, you may not use a particular card for long. In such a case, the credit card company or the bank may restrict transactions on the bank. This is to prevent unauthorized use of the credit card.

If the bank has disabled the credit card, the easiest way is to call the bank or reach through other channels to activate the credit card.

Entering incorrect credit card details in case of an online transaction

Always check twice before hitting the Pay button in an online transaction. It’s very easy to fill in the credit card details incorrectly in the payment details while shopping online. Especially, if you are using a mobile device to make a payment, say on amazon.com or an airline website the credit card declined may be due to entering incorrect details more often.

Some credit cards have dual-factor authentication, wherein you may have to enter an OTP (or a one-time password). This OTP may be in a form of a numeric code sent to a cell phone or an email id. Always, double-check the details as well as the OTP.

Things to keep in mind to prevent the credit card declined

We all can be a little proactive and keep a close tab on our credit cards. This would help us navigate any payment trouble or card declined scenarios.

Keep a sufficient balance on the credit card

Always keep a sufficient balance or credit limit on your credit card. It is also a best practice to maintain a good credit score to keep the overall credit utilization ratio below 30%. Read more to know about some of the other factors which help to keep a good credit score.

Online Shopping

If you are fully utilizing your credit card limits every month, it would be difficult to keep track and you may face a transaction decline due to credit limit.

Opt-in for notifications services for your credit card transactions. Credit card companies provide an option to send you reminders if you are hitting your credit limit or max allowed balance.

Manage your credit limit to keep your balance below the same

Do not overshoot the credit limit of your credit card. Ideally, keep the credit utilization ratio below 30%. This will help keep the credit score of the user healthy. High utilization of credit cards may put a dent in the credit score.

Also if you are making a usually large purchase on your credit cards, do inform the bank or card issuer beforehand. They will honor a valid transaction if it is within your credit limit. In case, you fear that you may shoot the limit. Do call them and request credit limit enhancement. Alternatively, make a part payment to restore your credit limit or balance.

Although, credit cards do allow increasing the credit limit temporarily. Enquire from your bank for the facility of over-the-credit limit access. Though, you may have to pay a one-time fee ranging from $35 – $49 to enhance this limit. Although, this credit limit does not get added to your overall credit limit. Your credit card will restore the original credit limit as soon as you pay off the bills.

Check beforehand doing international transactions

Enable foreign currency or international transactions before using your card internationally. Also if you have to make payments in foreign currency online, ensure that international transactions are available.

A plane

Customers can enable the foreign transaction from the issuer’s website or mobile app. Alternatively, they can also call the issuer bank for enabling foreign currency transactions.

Keep a note of the last date or expiry date of the card

Always note the credit card’s expiry date. Credit card companies or issuing banks will reach out to you before the card’s expiry date. Ensure that your contact details such as email address, home address, and mobile phone numbers are up to date. Normally, they will reach you through the number or email registered with them. If any is changed, do update them with the bank.

If you are not using a credit card. Another good practice is to cut the older physical credit cards. Cancel the older credit cards with the issuers.

Keep using your credit card

If you have lots of credit cards, keep rotating the cards and use other cards. Normally, people keep one primary credit card for transactions and one secondary credit card as backup.

A good practice is to cancel cards not used frequently. Additional credit cards do not add any value but may affect your overall credit score. To know the best practices to build a credit score.

Credit cards are an essential part of many people’s financial lives. They are also an important financial instrument. They offer convenience, flexibility, and rewards. But what exactly are credit cards and how do they work? In this post, we’ll explore the basics of credit cards. We will also explain how they can help you manage your money and build your credit score.

With all good things, there are some bad ones as well. The same is the case with credit cards. Indiscriminate high usage of credit cards and carrying balances can affect credit scores. Credit cards carry one of the highest interest rates on loans. These may be recipe for disaster for users as this may add to their debts.

To read about more basics of credit cards, please do read below:

First, let’s define what a credit card is. A credit card is a debt-based financial product. A credit card offers revolving credit limits to the issuer. The borrower or the credit card member can use the credit limit to make payments. They can use credit cards for shopping, dining at restaurants, and buying things online or at-store. The credit card company will send the member a bill for their outstanding balance.

Cardmembers will have to pay a minimum balance amount. If the member pays the bill in full in advance, their credit limit is restored and they have to pay no fee or interest. If the card member does not pay the balance, they will have to pay an APR (Annual Percentage Rate) and other late payment charges.

A credit card lets a credit card member borrow money and pay it back later. This means you can use a credit card to make purchases even if you don’t have the money in your bank account at the time. The credit card you use will determine how much you can borrow and the interest rate you’ll pay. Credit card companies are businesses that issue cards with specific terms and conditions.

Amex Membership Rewards

When a card member uses a credit card, they’re taking out a short-term loan from the bank. The loan is from the issuer of the credit card issuing bank. As a customer of the credit card, you have a fixed period usually 25 days to pay the balance in full. A Card member has to pay late payment fees if they do not make the payment in time. The bank will charge APR on the amount as well. The interest rate on a credit card depends on the type of card and the creditworthiness of the card member.

Who are the different parties in a credit card?

Credit cards are a loan from the issuing banks to the card members. Unlike a personal or consumer loan, the credit card offers the flexibility of use. There are many parties in play with a credit card.

Firstly, the borrower or the card member who applies for the Credit Card. The card members apply for the credit card and sign the card member agreement. A Credit card is a form of loan from the card issuer bank to the card member. They will check for the credit score of the card members before issuing the credit card.

Next, issuing Bank that issues credit cards. They govern the payment terms, and applicable interest rates, and provide credit risks.

Credit cards come printed with the names of other financial institutions. These include American Express, Visa, Mastercard, or Discover. These are the payment networks. These payment networks help clear payments while card members use their cards worldwide.

Further, there are also co-branded credit cards by airlines, hotels, retailers, and other issuers. These co-branded cards provide bonus rewards to card members. These bonus rewards are applicable only to the issuing brand.

Key advantages of using Credit Card

Flexibility

Compared to debit cards, credit cards also offer great flexibility. A member is always limited with the balance in the checking account for spending. The spending power is equal to the money in hand. On the other hand, with a credit card, a card member can spend money on the basis of their credit limit.

Credit cards have a credit limit and card members can spend up to that limit in a given billing cycle. Further, they can use their credit cards to make emergency purchases. They can indulge to pay for things they can’t afford at the moment. They may not have that money available to them right now. Members can spend the money on credit cards and pay it on a fixed date as per the terms and conditions of the credit card.

For payments credit cards also offer flexibility. Card members can pay off the balance in full each month. They can also pay the amount in payment plans over months by paying the applicable APR or interest rate. Some credit cards also levy late fees and other charges on delayed payments. Always be conscious of spending money on a credit card. Do not get into the trap of spending too much.

Protection

Another, important key advantage of using a credit card over cash is an offer of a greater level of protection. When a customer buys something using a credit card, they are protected by the Fair Credit Billing Act. This law requires merchants to correct any errors on the credit card bill. It also gives the cardmember the right to dispute any charges they didn’t approve.

Rewards

Another important and lucrative advantage of using a credit card over cash is that it allows one to earn rewards. Credit cards have programs to offer rich rewards. Reward programs allow card members to earn points, miles, or cash back on their purchases. This means that every time a member uses their credit card, they’re also earning rewards.

Credit cards

Credit card issuers offer multitudes of rewards which may include:

Airline miles with the airline and bank co-branded credit cards

One-time bonus points or statement credits on new cards issuance

Introductory low or even 0% APR on balance transfers or new purchases

Bonus points on the anniversary of the cards for paying annual fees

Free nights on co-branded hotel cards

Faster points or miles on specific spend on dining out, travel, or streaming services

Access to airport lounges on airline or travel credit cards

Statement credits against fees of incidental charges on airports and other airport services

Credit Score

Besides the above advantages, using a credit card can also help build a card member’s credit score. A credit score or the most popular version FICO score is a three-digit number. This number reflects the creditworthiness of a customer.

A variety of factors affect the credit score of a card member. These include payment history, credit utilization ratio, credit mix, and credit history. It’s used by lenders to determine whether to approve them for credit and what interest rate to charge.

When a member uses a credit card, they’re building a credit history. This is an important factor in determining their credit score. Credit card companies report to the bureaus about the usage of cards, and late, or missed payments. As long as you make your payments on time and don’t exceed your credit limit, your credit score remains great. By using credit cards in a responsible manner, members can improve or build credit scores.

Always pay your credit bills on time and in full to the extent possible. I have personally had the misfortune of getting slapped with a late payment fee as well as credit bureau reporting for getting late for a single day. This is after I have a spotless history of on-time payments for more than 5 years.

Credit card usage

Cash advance in a credit card

A cash advance is a facility to take advance cash from a credit card. A participating ATM can dispense this cash. This cash is a loan from credit card issuers and charges interest. There are fees for using this facility. The cash advance also carries higher applicable interest charges. This is a great facility in case of emergency or pinch. Do not take cash advances as a practice. It not only affects one’s financial goals, but a missed payment may also affect your credit score.

Shortcomings of Credit Card

There are several disadvantages or shortcomings of using a credit card. Firstly, it is a great financial product with ease of use. On the other hand, it is a disaster in hands of an overspender. For a shopaholic credit card is a path to Nirvana. It can fuel the endorphins of the shopper but may push them into the credit card debt trap.

Credit Score deterioration of the card members

High usage of credit cards can affect the credit score of members. If they consistently carry a high balance or make late payments, their credit scores may suffer. For a business loan or a mortgage, a good credit score is essential. A lot of young adults spoil their credit scores through the indiscriminate use of credit cards. Later when they actually need a loan they struggle.

Interest Rates and high fees

Credit card issuers charge high fees and interest rates on unpaid balances. They often come with fees, such as annual fees, balance transfer fees, and cash advance fees. These can pile on if a user is dependent on credit card debt. This can spiral out of control and leave unsustainable levels of debt.

Fraud

Additionally, credit cards are vulnerable to fraud and identity theft. They can cause financial and personal stress if you fell prey to the same. Always practice safe card usage. Read more for details on how to use your credit card safely.

Chase Bank is one of the largest financial institutions in the USA. They serve almost half of the US population with their products. Chase offers a variety of products such as Chase rewards credit cards, checking accounts, ATMs, Debit cards, mortgages, loans, and other financial products. JP Morgan Chase and Company is the parent company of Chase Bank.

Chase offers a number of Rewards credit cards. They also offer co-branded credit cards with Marriott Bonvoy, United, Southwest, and Air Canada airlines. Chase also offers co-branded credit cards with Amazon. Finally, to know more about shopping credit cards read our post.

Chase Rewards Credit Cards Advantages and Offerings

Chase Rewards offer a number of advantages to credit card members. Some of these include.

Zero Liability Protection

Chase Rewards credit card offers zero liability protection. Members are not responsible for any unauthorized charges made with their card or account information. They have to call Chase Credit cards to report any theft or loss of the credit card.

Purchase Protection

This card also offers Purchase Protection for new purchases for 120 days. Any new purchases made on the card are covered for $500 of theft or damage claim. Every account is covered for a sum of $50,000.

Auto Rental Collision Damage Waiver

Chase Rewards card offers Auto rental collision damage waiver. Members have to decline the rental company’s collision insurance to qualify. They need to charge the entire rental cost to their card to qualify for the damage waiver claim. Coverage is provided for theft and collision damage for most cars in the U.S. and abroad. In the U.S., coverage is secondary to personal insurance.

Extended Warranty Protection

Chase Rewards credit card extends the time period of the U.S. manufacturer’s warranty by an additional year, on eligible warranties of three years or less. This is nifty for new purchases, especially for electronics and appliances.

Trip Cancellation

Further, Chase credit card offers Trip Cancellation and trip interruption Insurance. To be eligible for this travel insurance the purchase must be made on the Chase Freedom Unlimited credit card. Although, the maximum reimbursement is up to $1,500 per person. There is also a $6,000 per trip restriction. To qualify, trips should be all pre-paid, non-refundable passenger fares.

Chase Rewards Credit Cards List

Herein, we will review the current Chase Rewards credit cards for their offers.

Chase Freedom Unlimited credit card

Fees: This credit card charges $0 in annual fees.

Intro Rewards: Cardmembers can earn a $200 bonus after they spend $500 on purchases in the first 3 months from account opening. They can also earn 5% cash back on grocery store purchases up to $12,000 spent in the first year. This offer excludes purchases at Target and Walmart. This amounts to a saving of $600 on everyday grocery purchases. Furthermore, this card offers an introductory 0% APR for 15 months on balance transfers and purchases.

Rewards: Cardmembers earn cashback of 1.5% for every purchase. Apart from this cashback, they can also win 3% cash back on dining and drugstore purchases. Dining rewards are available for dining at restaurants, takeout, or even delivery from restaurants. Members can win 5% cash back on travel bookings through Chase Ultimate Rewards.

In a nutshell: The Chase Freedom Unlimited Credit card is one of the best rewards cards in the market with $0 annual fees. It offers a flat 1.5% cashback on most purchases. It also offers additional cashback on other categories such as travel, grocery, drugstores, and dining out. Finally, this card is a 0% introductory APR credit card. It offers this 0% APR for 15 months.

Chase Freedom Flex Credit Card

Freedom Flex

Fees: Chase Freedom Flex credit cards charge $0 in joining and annual fees

Intro Rewards: This credit card offers a $200 bonus on a spend of $500 in the first three months of the card approval. It offers a 0% introductory APR for 15 months on balance transfers and purchases.

Rewards: Freedom Flex offers 5% cash back on purchases from grocery stores, gas stations, and select online merchants. Further, it also offers 5% cash back on travel purchased through Chase Ultimate Rewards

In a nutshell: Chase Freedom Flex Card offers excellent rewards on everyday purchases categories. For example, groceries, gas, and online merchants. It also offers 5% cash back on travel through Chase Ultimate Rewards. This card also offers a 3% cash back on dining at restaurants and drugstore purchases. For the other purchases, there is a cashback of 1%.

Cash back never expires on this card. This card also offers Zero Liability protection and purchase protection. Further, other additional offers and benefits are available from Mastercard.

Chase Sapphire Preferred Card

Sapphire Preferred

Fees: Annual fee of $95 and a 3% introductory balance transfer fee which increases to 5% of the balance transfer fee

Intro Rewards: 60,000 bonus points after the card member spends $4,000 on purchases in the first 3 months of the new card opening. These bonus points are worth $750 when redeemed for travel through Chase Ultimate Rewards.

Rewards: This credit card offers $50 statement credits every anniversary year for hotel stays purchased through Chase Ultimate Rewards. This card also offers 5x total points on all travel purchased through Chase Ultimate Rewards. Card members can also earn 2x points on airfare, hotel booking, and taxis. Card members can earn 3x points on eligible online grocery purchases and on dining and takeout from restaurants.

In a nutshell: Chase Sapphire Preferred is a great travel rewards credit card. Read more to know more about the best travel credit cards. The best part about this credit card is the bonus anniversary points. Each anniversary year the card member is eligible for 10% of bonus points of the total spent in the last year. If a customer made a purchase of $10,000 in a year, they are eligible for 1,000 bonus points. This card offers discounts or membership benefits from several other companies like Doordash, Instacart, Lyft, etc.

Amazon Prime Rewards Visa Credit Card

Amazon Prime Rewards

Fees: $0 with a valid Amazon Prime membership

Intro Rewards: Card members earn a $150 welcome Amazon Gift Card upon approval of a new credit card.

Rewards: Further, members earn 5% back in rewards on Amazon.com and Whole Foods Market. They also earn 2% rewards in restaurants and gas stations. Finally, they receive 1% reward on the rest of their purchases.

In a nutshell: Firstly, this card requires the card members to have a valid Amazon Prime membership. This is good for existing card members. The current cost of the Prime membership is $39 per month. Chase and Amazon also offer another credit card Amazon Rewards Visa Card. The card doesn’t require a Prime membership but it also offers lower rewards.

Card members can redeem the cashback on Amazon.com or they can select to redeem it for gift cards, travel, or dining deals on Chase Rewards. Finally, this card offers the card members complimentary Visa Signature Concierge Service 24 hours a day.

Chase Freedom Student Card

Freedom Student

Fees: This card has no annual fee.

Intro Rewards: Card members earn $50 bonus on making the first purchase within 3 months of card opening.

Rewards: Chase Freedom offers very little incentive to users. For instance, it offers a measly 1% cashback on all purchases. On the other hand, the main advantage of this card is the high acceptance rate for students. Chase Freedom Student Card provides free access to credit scores as well.

In a nutshell: No credit score is required to apply for this card. This is a good starter credit card to build credit over time. This card rewards making timely payments by increasing the credit limit. They also provide a good standing reward of $20 each anniversary year for 5 years.

Credit cards for fair credit or average credit can help people to build their credit. These credit cards usually come with $0 annual fees. They report the monthly payment fees to three credit bureaus and help build the credit score. Further, these credit cards also have credit-building features such as providing access to free credit scores. Finally, these credit cards also offer education on building good credit scores.

With an improved credit score members can have better rates on loans and mortgages. Credit cards on offer for Fair credit offer better features than secured credit cards.

How to monitor your credit score to help improve it from Fair to Good?

Cardmembers can opt for a service like CreditWise from Capital One. This service provides the credit score of a user from the TransUnion Credit bureau. It is available for any adult with a valid social security number. There should be an available file with the user with TransUnion for this service to work. There is no requirement to be a Capital One customer to use this service.

Credit cards for people with Fair Credit Scores

#1 CapitalOne Platinum Mastercard

Fees: This credit card is available with $0 in annual fees. It also offers $0 foreign transaction fees.

Joining Rewards: This credit card doesn’t offer any joining rewards.

Rewards: Mastercard offers $0 Fraud Liability if the card is ever lost or stolen. Capital One has a tool to monitor the credit profile of a user. Card members get unlimited access to their credit score CreditWise from Capital One.

In a Nutshell: This is one of the best credit cards for members with Fair credit. This card automatically increases the credit limit of the user over time. They consider increasing the credit limit starting in 6 months. They take into account payment history patterns to raise the limit. This is a great credit card for a starter person looking to build credit.

#2 Milestone Gold Mastercard

Fees: Milestone offers multiple gold cards. The annual fee of the credit card varies from $35-$75 and it depends on the pre-qualification and approval of the card. Members can pre-qualify for a Milestone credit card to check for eligible fees and APR.

Rewards: The Milestone credit card is a special financial product for rebuilding or building credit. It can be used as a credit card wherever Mastercard is accepted. Unlike a secured credit card which may require a security deposit. Milestone credit card is a good option in place of a traditional secured credit card.

In a Nutshell: Milestone Gold Mastercard is a good starting product for anyone who is interested in establishing or rebuilding their credit. They report the account history to all three major credit bureaus. They give cardholders a chance to establish a consistent payment record. This helps in building credit scores over time.

Milestone is a limiting credit card as it doesn’t offer too many rewards or facilities. But its sole purpose is to build a credit score. It does not offer a facility for a balance transfer on their credit card. International transactions on the Milestone Gold Mastercard are disabled by default.

#3 Mission Lane Visa Credit Card

Fees: Mission Lane Visa credit card has an annual fee of $59.

Rewards: This credit card doesn’t offer rewards as the intent of this credit card is to rebuild credit.

In a Nutshell: Mission Lane Visa Credit Card is a credit rebuilding card. It doesn’t require a security deposit to offer a credit card. Once the credit card is approved by Mission Lane, they offer a very high APR loan. Mission Lane credit card offers a limited credit limit for the card members to start with. This credit limit may be $500 or $800 for a card member. Once a member makes their payments on time for a few months, Mission Lane increases the limit on the credit card.

Mission Lane reports the payment history to all three credit bureaus. It also provides free anytime access to the credit score of the card member. Access to this credit score helps the cardmember take control of their finances. This credit card doesn’t offer any balance transfer facility. The credit card comes with an app to monitor the financial progress.

#4 Petal 1 Credit Card

Fees: Petal 1 credit card is a no-fee credit card. It charges no annual fees and no foreign fees.

Rewards: Cardmembers can earn 1.5% cash back on all purchases. It also offers a high cashback of upto 10% on selected merchants.

In a Nutshell: Petal 1 credit card is a great card to build credit as well as earn rewards. Members start with a starting credit limit. They can increase the credit limit with monthly payments on time. Petal 1 credit card reports to all three credit bureaus.

Are you looking for a guide on how to select best credit card for yourself? We bring you our expert question base guide to select the best credit cards in 2023.

If anyone looks in their wallet, they will easily find 5-8 credit cards. Everyone is just obsessed with these plastic shiny cards. The United States of America has one of the highest credit card ownership. We have more than 900 million credit cards outstanding in 2022. On average, every adult American owns 5.5 credit cards. We also carry huge trillions of US dollar balances on our credit cards.

People select a new credit card for a number of reasons!

Reasons to select best credit card

They may see great rewards from the card

Looking to build credit score over time

Using credit cards to revolve money before a paycheck arrives

The convenience of using cards against carrying cash

Traveling for pleasure or business

Spending on business spends which will get reimbursed in some time

Whenever you face the choice of selecting one more card, how do you select it? Do you choose the card rationally? Do you select a credit card because you need to have it? Or you are too polite to refuse a pushy salesman at a checkout counter. Whatever triggers you, always do a thorough analysis before selecting a credit card. Do not let your emotions trump your financial goals by getting into the trap of too many cards.

Whenever a person applies for a credit card, the credit card agency does a hard pull on the credit score. This affects a person’s credit score negatively. Too many open credit cards also affect the credit score. Also, it’s practically difficult to manage too many credit cards.

So, if you have decided to go for a credit card and are sure of it. We have listed some of the below criteria to help select you a credit card easily. Ask yourself the below questions to narrow down the credit card.

What are your needs for a credit card?

You should, first of all, identify the need for a credit card. Is the card going to be your primary card or you are choosing a secondary card? Members should always be sure what the primary use of the credit card they are applying for is. Do not apply for a credit card at the insistence of a sales representative or a friend.

Select a card on the basis of its merit. If you are looking for a rewards credit card. Select one of the best rewards credit cards. Frequent travelers should opt for travel focus credit cards. They can select co-branded cards from airlines or hotels. These credit cards offer rewards favoring travelers. For example, access to airport lounges, free check-in luggage, priority boarding, early check-ins, and late checkouts at hotels.

If a person shops from a specific retailer, they should select the credit card from them. This would help them in maximizing rewards from the chain of these retailers. This can also help them with other benefits like free shipping, extended returns, or exclusive access to discounts. Read more to know the best credit cards from retailers.

Identify your credit score to select best credit card

It’s good to start from the basics, what is your current credit score? Members may want to build their credit or they may look to select one of the best credit cards to build their credit score. Read on to know more about improving your credit card score here.

Students may opt for Student credit cards. These are specially designed for students registered in a US university or school.

Top rewards cards or some of the premium credit cards require a high or excellent FICO score. It is best to apply for these credit cards only when you have a such high credit score. They easily reject people with a fair or average credit score.

Card members should monitor their credit scores regularly. They can either get a free credit score from their credit card. Or they may access free reports once a year from all three credit rating agencies viz. Experian, Equifax, and TransUnion. They can also access free credit score copies from AnnualCreditReport.com. This is a federal government-controlled site that provides consumers with access to a free copy of their credit reports each year. The reports are available from all three credit bureaus.

What is your typical credit card use?

The market is full of all sorts of credit cards. Always select the credit card which helps you in the best possible way. The card should add value to the user and should help with their financial goals. Adding a credit card should not add worries. Also, it should not increase your debt levels.

Students or credit-building adults

Students or credit-building adults could opt for secured credit cards. These credit cards take a security deposit and provide a credit limit. The credit limit is equal to the security deposit. Once you start paying back for the payments, the bank will report the payments to the credit bureaus. This will help in building the credit score of the member.

Everyday purchases

Rewards credit cards are best for everyday purchases. These everyday purchases may include groceries, gas, utility payments, streaming services, internet, and other online or in-store shopping. Reward cards offering cash back either directly in form of statement credits or points are best bets for such purchases. Rewards credit cards should always be the primary card to maximize rewards and value.

Balance transfer or 0% APR credit cards

Cardmembers with a balance on their credit card can look to opt for balance transfer credit cards. These credit cards provide better APR and lower interest outgo. Similarly, 0% APR credit cards offer introductory offers on new purchases or balance transfers. They could be excellent instruments to reduce overall interest outgoing by taking advantage of intro offers.

How much does this credit card cost me in fees?

Credit card charges a number of fees. For instance, annual fees, balance transfer fees, APR on outstanding balances, and late payment charges. They may also charge access fees for using certain services. Normally, credit cards also charge international transaction charges. These are currency conversion charges for using the card outside the USA.

Users should be aware of various fees applicable to their cards before applying for the same. Check the credit card issuer’s website to know the applicable fees. Also, check the rewards offered by the credit card. Some rewards are introductory and available one-off. Don’t be lured by such one-off rewards. Look for the overall value offered by the credit card.

What are the signs to avoid a credit card?

Sometimes not doing something is better than taking the step. Do not apply for a credit card and look for the following signs.

Accepting a credit card because your friend has recommended it. No harm in taking advice from a loved one. But do your own due diligence. Your financial situation, goals, and paying capacity might not be the same. Applying for a credit card with a $400 annual fee doesn’t make sense. The prime feature of the card may be access to Golf courses. Unless you play golf or visit golf courses doesn’t make sense for you.

If you already have several credit cards. Do not add more credit cards. Close the existing credit accounts before opening a new one. Credit card companies take a negative view to too many credit cards. They consider sucha person at ta risk of default. Also, utlize the limit of your credit cards judiciously. Keep the utilization ratio of the credit cards to below 30%.

Have you got the shiny new card? What Next?

Once you have got a credit card in your hand, always enable the SMS or app notification of the credit card provider. This will ensure that you are using your card safely and you get notification is any unauthorized charge is made on the card.

Always pay the balances on time and in full. Monitor the credit report periodically, for any change. A healthy financial life is important to keep up your mental health.

Gas is an everyday expense for everyone. Popular gas station service providers partner with Banks and Credit card services to issue these credit cards. These co-branded credit cards provide discounts at gas pumps, marts, or convenience stores in gas stations.

The USA is one of the most gas-guzzling countries. Road transportation on our highways is the preferred means of transportation. Motor gasoline is one of the major fuel consumed in the USA. A lot of people in the USA prefer road trips and they keep on consuming gasoline. As per an estimate by the US Energy Information Administration, US travelers spent 135 billion gallons of gasoline in 2021. This amount to 369 million gallons of gasoline per day. Light duty vehicles such as personal trucks, cars, and sport utility vehicles consume 91% of this gasoline.

Shell is the major fuel station service provider in the USA currently. They have more than 12,400 locations all across the USA. Exxon Mobil is a close second with almost 11,900 locations. Next, comes Chevron with 6,990 locations across the USA.

How do Gas stations make money?

Gas stations make most of their profits in the convenience stores next to the gas pumps. They keep the gas price competitive with razor-thin margins to cover the cost of rent, labor, and utilities. Gas stations make the most money off food and drinks including alcohol sales. They sell food and drinks at a premium as customers usually buy food and drinks on their trips from them. They can also make money offering insurance, cleaning services, car repairs, and other associated services.

Here we will review some of the co-branded gas station credit cards for our readers.

#1. Shell Fuel Rewards Mastercard

Joining Rewards: Customers can save 30¢/gallon up to a total of 35 gallons. This saving is valid on the first five fuel station purchases for new customers.

Rewards: Members save 10¢/gallon on all purchases at Shell gas pumps. Cardmembers can also earn 10% Shell rebates on their first $1,200 Shell non-fuel purchases per year. They can also earn special rewards on other marked products in Shell convenience stores in the stations.

Further, cardmembers can earn 2% Shell rebates on their first $10,000 Dining and Grocery purchases per year. They can also earn 10¢/gal for every $50 spent at participating restaurants with a linked credit or debit card. Members can select the participating restaurants and keep earning rewards. Additionally, members earn 1% Shell rebates on all other purchases. Members can also earn rewards for every $50 spent shopping their favorite brands at fuelrewards.com/shopping.

In a nutshell: Though it may appear that the savings are 30¢/gallon and may amount much, it is just $10 for 35 gallons of purchase. Again the 10¢/gallon is just 2% of the total savings if gasoline is priced at $5/gallon. Cardmembers can get better overall rewards with a Rewards credit card.

#2 Exxon Mobil+ Credit Card

Joining Rewards: Cardmembers earn up to 42¢/gallon for the first two months. Further, members earn 30¢/gallon as a bonus statement credit on fuel for their first two months after the account open date.

Rewards: Members can get 12¢/gallon in instant savings on every gallon of premium gasoline. They will receive 10¢/gal on other grades of fuel every time. Additionally, cardmembers receive 5% statement credit for all in-store purchases and car washes. Though, this reward has a limit of the first $1,200 in non-fuel purchases per year.

In a nutshell: Exxon also provides 2% rewards on their credit card. Additional statement credit is also limited to $1,200 per year. This amounts to 5% of $100 per month, which is a measly $5. Though this is free money, a member needs to spend $100 in the gas station store every month. It is better to fuel oneself at a better food restaurant or a supermarket.

#3 BPMe Rewards Visa Signature Card

BPME Rewards Card

Joining Rewards: Members get 30¢/gallon for the first 60 days of opening a new BPMe Rewards Visa Signature credit card.

Rewards: Once the 60 days period is over, members get 15¢/gallon. This credit card also provides 3% cash back on dining in restaurants, takeout, or delivery. Further, they also get 3% cash back on groceries. Cardmembers also get 5% cash back on all non-fuel purchases at BP and Amoco fuel stations. For the rest of the purchases earn 1% cash back rewards.

Members also receive other Visa Signature benefits. These include Purchase Protection on qualified purchases. Zero liability for a stolen or lost credit card. Contactless, tap-and-go credit cards.

Cardmembers can redeem their rewards for statement credit, gift cards from major retailers, travel experiences, and more.

In a nutshell: BPMe Rewards card offers better rewards at 3%. These rewards are useful and even better than other rewards credit cards. To know more about rewards cards, do read our take on the best rewards credit card.

Another advantage of this card is that the rewards can be redeemed for statement credits or gift cards. Usually, other gas station cards will make you use the rewards only for fuel purchases. Here, flexibility is better.

#4 Costco Anywhere Visa Card by Citi

Costco Citi Visa

Joining Rewards: There are no special joining rewards on this credit card as of now.

Rewards: Card members earn 4% rewards on the gas and EV charging up to $7,000 per year. In addition, they can earn 3% rewards on restaurants and travel. Further, 2% rewards on eligible purchases in Costco stores and Costco.com and 1% rewards on all other purchases.

Costco offers members exclusive discounts for credit card holders. Card members can add more family members to these cards, and they can earn cashback on their purchases as well. Finally, Card members can redeem cashback against an annual certificate for redeeming merchandise at US Costco stores. In a nutshell: This credit card costs $0 in fees with an existing paying Costco membership. Further, card members do not need a separate membership to Costco. The credit card works as a Costco membership card. This credit card makes sense for all purchases on Costco, not only the fuel. Members earn 4% rewards on fuel limited to $7,000 purchases. This comes to $280 in a year.

Credit score for beginners is a debatable topic. A credit score is an important financial scorecard. A good credit score helps a person apply for mortgages or loans at a better rate. Credit agencies consider the credit score of a customer to provide the APR rate for credit cards, loans, mortgages, and other credit lines. Credit scores are determined by the FICO score. For a new person in the USA or for a new adult, this is important. Additionally, building a responsible credit score is a crucial first step in their financial journey. They need to find a way to develop a good credit score.

Developing and maintaining a good credit score is a mindset as well. In order to, develop a mindset is the first step. For instance, spending money on a credit card is easy. On the other hand, developing a habit to pay credit card bills on time is tough. Keeping an eye on the credit score and credit history is also very important.

Herein we will delve into some of the ways, new adults or members can develop a credit score and credit history:

Open a Secured Credit Card to build credit score for beginners

The easiest way to build a credit history for a beginner is to open a secured credit card. Although, secured credit cards are good for rebuilding credit history. Alternatively, they can also be used for building credit history from scratch. Secured credit cards provide a credit up to the security deposit with the credit card company. For people migrating from other countries to the USA, the secured credit card may be the approach to building credit over time.

Discover Credit Cards

Card members need to be careful and pay all the dues on time for a credit card. This credit card is for building credit scores and should be used for the same. It should never be used for a stop-gap arrangement or rollover credit.

People residing in the USA, having a Social Security Number (SSN), and having a valid checking account can open a secured credit card with a bank. It’s always good to check with the issuing bank to know the exact requirement. To know more about secured credit cards read best-secured credit cards.

Opt for a Student Credit Card if you are a student

These credit cards are great for students who are over 16 years of age. These students are also developing a new credit history for themselves. They can opt to apply for a student credit card.

Student credit cards are specially designed for students with Zero Credit history. Thus, they require the cardholder to be enrolled in a student program in a college, university, or community college. Some student credit cards may also require a credit deposit or annual fee. It’s always good to look for credit cards with zero annual fees. Additionally, they may also offer rewards and perks for the students. Some of these include cashback or rewards on purchases.

In the end, these credit cards can help students develop a credit history. They will also learn to manage their finances better.

Retailer credit cards are fairly easy to get. They want you to spend money in their stores. Retailers issue two types of credit cards. Firstly, they issue in-store credit cards. This credit card works in specific retail outlets. The next one is credit cards with Visa or Mastercard. These work as normal credit cards. It’s always good to check with a retailer for their terms and conditions. They will help a customer build a credit history or credit score over time.

Gas station credit cards are also a good place to start for beginners. They are fairly easy to get for people with fair or bad credit and sometimes no credit. Gas station credit cards are good for small everyday purchases. They also help a customer instill a habit of financial prudence.

Customers can also co-sign for a loan application. Prime borrower takes the loan and can sign a co-signee for the same. A working spouse, parents, or a friend can be a prime borrower. Once the original borrower starts paying the loan back, the creditor will update the credit bureau for both borrowers. This could also be a way to build credit scores over time. As the loan will be paid over time, the credit score will also build over time.

Although, this facility should be used with caution. If the borrower doesn’t have enough money and defaults. The non-payment will also affect the co-borrower. It’s better to rely on someone within the family or a close friend whose financial situation one is aware of. Instead of helping in building a credit score, these may do harm in the long term. Thus, be careful before signing the loan as a co-borrower.

Use a credit-building service for improving credit score for beginners

Another great way to establish a credit history is to get a secured credit-building service. Examples of such services Kikoff, creditstrong, and Self. These credit-building companies provide customers with a revolving credit line against security. Security could be in the form of a deposit for beginners. They do charge fees for providing these services. They report to all three credit bureaus. Using these services can help customers build credit history over time.

When customers make scheduled payments they are reported to the credit bureaus until the amount they owe is paid back. The deposit is then released back to them after the account is closed. Once a customer has proven that they can pay back the loan, their FICO score may improve and credit card issuers can be quick to offer credit.

Report Rental and Utility Payments

Rental payments are also part of payments to a realtor or landlord on a property. These payments are some of the biggest expenses per month. There are services like Experian RentBureau which can help you build a credit history on paying rent on time. Similarly, there is another service Experian Boost which can help boost credit scores on utility payments. These include payments for internet or mobile bills. Experian boost also works with even streaming services like Netflix and Disney+. Experian Boost is a free service to customers.

Good practices for building credit score for beginners

Always pay your credit card and loan EMIs on time. This is the number one criterion in any credit bureau’s score and it affects the credit score. A delay in payment by the customer is informed to the credit bureaus, and it may straightaway affect your score.

Always keep the credit utilization ratio of your open credit like credit cards to a minimum. Ideally, the credit utilization ratio should not go beyond 30%. It means, that if you have 2 credit cards with $4,000 and $2,500 credit lines. The total credit limit would be $6,500. Always keep your overall spending combines on credit cards below $1,950.

Keep a close eye on the credit report. Customers can request their credit report for free from AnnualCreditReport.com. They should monitor for any change not initiated by them.

Credit score and history take time to built. A person should look at it from a long-term perspective. As a result, rushing into things might not help. Do not fall into trap of some companies which give shortcuts to improve or build credit score.

The Hilton Honors is the loyalty program from Hilton Hotels. Hilton is a global chain of more than 7000 hotels globally in more than 120 locations of the world.

Hilton offers lots of ways to earn and use Points every day for their loyalty program members. Loyalty Members can start earning points on every dollar spent, the moment they sign up for Hilton Honors. There is no limit to the number of Base Points a member can earn. Additionally, they offer co-branded credit cards with American Express. Members can earn exclusive elite benefits and earn even more points with these credit cards.

Earn Hilton Honors Points

Members can win points on their room rates as well as the total folio charges. Total folio charges include other incidentals charged to the room. The incidentals include dining, telephone, laundry, pay-per-view movies, entertainment, and recreational facilities. Any applicable federal, state or local tax is excluded from any earning points.

Further, members can earn 500 Bonus Points when they join the Hilton Honors Dining Program. In order to qualify they need to spend $25 at participating restaurants. They need to complete an online review in the first 30 days of activating the membership. In addition, they earn Points for every $1 spent at participating restaurants, bars, and clubs.

Members can also earn points when they sign up for Guest Opinion Rewards. This is an online portal that helps Hilton hotels to collect member opinions. First-time users get 1250 points for participating in the first survey. Then earn Points for each additional survey.

Additionally, Hilton Honors Members can earn up to 5,000 Points on qualifying car rentals. The qualifying car rental companies include Alamo, Enterprise, and National.

Hilton Honors permit members to buy Points. They can buy up to 80,000 Points in a calendar year. They can also exchange Points. Hilton Honors points can be transferred as well. Members can also pool points in a single account. Further, they can use the Pooled points to book a stay together.

Hilton Honors membership tiers

Hilton Honor offers membership tiers. Each tier offers rewards of amenities, bonus points, and enhanced experience. Qualification to these tiers depends on the number of nights of stay or points earned. Members may earn a higher Elite status when their stays, nights, or Base Points are in a calendar year. To qualify the Member for the next tier they need to maintain the same spending.

Once a Member reaches a certain Elite tier, they may keep the such status for the calendar year in which the Elite tier is earned and the subsequent calendar year. Hilton Honors have a membership tier and other Elite Tier status. The Elite tier status includes Silver Elite Member, Gold Elite Member, and Diamond Elite Member status.

Member Tier

This is the starting default tier for all customers joining the Hilton Honors program. Members earn rewards points on every stay with Hilton Hotels or resorts. For every $1 spent in hotels, they earn 10 points. The award of points on certain brands They can use these points for free nights, travel experiences with partners, exclusive experiences, or more.

Members receive an exclusive rate when they book on Hilton.com or the Hilton app. Hilton provides digital keys to the members for all hotel rooms. They can use the Hilton Honors app on their phone to unlock their room doors. Members can redeem their rewards for free nights for room bookings in Hilton Hotels and resorts. As members, the resort fee is waived on redeeming nights.

Hilton Booking

Members can also use the Hilton Honors app to do digital check-in or checkout from anywhere. They can also choose any room of their choice up to 24 hours in advance. They can also use complimentary wi-fi throughout the hotels.

Silver Elite Tier

This is the 2nd membership tier in the Hilton Honors membership program. To reach this level, members need to spend 10 nights and complete 4 stays with Hilton. They can also achieve this status by earning 25,00 points.

Silver tier members inherit all the benefits of the membership tier. Apart from the above benefits, they also get 20% bonus points on every booking. Members also receive complimentary 2 bottles of water when they arrive (at select hotels). They also get the fifth night free on booking a stay with Hilton Hotels for four nights. This needs to redeem points for this four-day stay. Additionally, these members enjoy 15% discounts on spas within the Hilton portfolio of brands.

Finally, they can roll over extra night credit to maintain or improve their status for the next calendar year.

Gold Elite Tier

Members spending 40 nights or 20 stays or 75,000 base points receive Gold Elite Tier with Hilton Honors. These members inherit all the benefits of the silver elite tier to their status. Additionally, they receive 80% bonus points on Base Points on their stays. Hilton will also offer an upgraded room subject to availability.

Gold Elite tier members receive MyWay benefits. As part of this benefit, they’ll receive a Daily Food & Beverage Credit at select brands in the U.S., and Motto by Hilton globally. They can also receive complimentary Continental Breakfast at select brands outside the U.S. This benefit is for the member and one additional guest registered to the same room each night of their stay. Gold tier members and one of their registered guests also get access to the Exclusive Lounge in the hotels. They should be staying on the Executive floor in the hotels.

Diamond Elite Tier

This tier is the highest membership status in the Hilton Honors program. Members spending 60 nights, 30 stays, or earning 120,000 base points will receive Diamond elite tier status. Apart from inheriting all the perks of the lower tiers, the diamond tier offers 100% Bonus Points.

Diamond members and one accompanied guest also get complimentary access to Executive lounges in the hotels. Members can relax and enjoy culinary delights and drinks in Executive lounges. These members also get complimentary access to Premium wifi at participating hotels. They also get guaranteed rooms in select hotels on a 48-hour period notice.

Hilton Spa and Experience

Members completing Diamond tier status for three years and staying 250 life nights. Alternatively, earning 500,000 base points get an extension of status for a year. This one-year extension doesn’t require any minimum criteria. Diamond members can give Gold status as a gift to any other member on hitting 60 nights in the calendar year. If the member hits 100 nights in a calendar year, they can gift a Diamond status.

Lifetime Diamond status is awarded to a select few Hilton Honor members. To achieve Lifetime Diamond status, a member has to reach some milestones. They need to keep the Diamond tier status for 10 years. Or they may have spent 1,000 nights in Hilton hotels. Alternatively, they might have earned 2 million Base Points.

Accrual of Bonus Points

Members earn a fixed amount of Hilton Honors Bonus Points after achieving eligible nights each year. They earn 10,000 Bonus Points at 40 eligible nights. Further, they earn 10,000 Bonus Points for every 10 additional eligible nights thereafter.

Members will earn an additional 30,000 Hilton Honors Bonus Points on their 60th eligible night per calendar year.

Within a calendar year, the maximum number of nights that a member could achieve toward these bonuses is 365 nights. These are equivalent to an additional 360,000 Hilton Honors Bonus Points per year. Milestone Bonuses are considered bonus points. Hence, they do not count as base points for the purposes of earning status for the calendar year.

Rewards and redemption of Points

Hilton Honors members can redeem their Points on a number of experiences of their choice. They also get access to Exclusive Hilton Honors Experiences. Members can redeem their reward points to bid on auctions to win these experiences.

Hilton Dining

Free nights

Members can redeem their Points to book free nights in Hilton Hotels and Resorts. They can book any combination of Points and money. The best part about the Hilton rewards is that there are no blackout dates. Members can choose any dates at their convenience and on the basis of their reward points balance. Hilton Honors Points can be earned for stays only at hotels within the Hilton Portfolio.

Experiences

Hilton Honor members get VIP access to concerts, dining, sporting events, and more with their Points. These exclusive events are usually placed in auctions. Members can put in bids to win access to these events. Hilton Honors Experience team reaches out to the winning members within 2 business days. They will confirm the identity of the member and issue the requisite tickets.

Lyft rides

Members can also link their Lyft account with the Hilton Honors account. They can earn points on Lyft rides. Members can earn 3 points for $1. They can also redeem the Hilton Honors Points to pay for rides.

Hilton Lyft rides

Shopping

Hilton also offers an online mall to redeem points. Members can select Shop with Points options to redeem points in the online mall. They can also redeem points on everyday purchases at Amazon.com.

Rental cars

Additionally, members can also redeem Points for car rentals with multiple rental car providers. For instance, Alamo, National, and Enterprise.

Airline transfers

Hilton also has partnerships with several airlines. Hilton Honors Loyalty Members can convert their Points into airline miles.

Hilton Honors members can also connect their Hilton Honors and Ticketmaster accounts. They can also redeem Points for live experiences like Live Nation concerts. Also games and other events on LiveNation.com and Ticketmaster.com.

Hilton Honors Co-branded Credit Cards

Hilton also has a partnership with American Express to issue co-branded credit cards. These credit cards offer users to earn Base Points. They earn points on staying with Hilton as well as on everyday purchases.

Hilton Honors Card

Hilton Honors Card

Fees: This credit card charges $0 in annual fees. It also charges no foreign transaction fees.

Rewards: Card members also earn 100,000 Bonus Points. They have to spend $2,000 in purchases on this credit card within the first 6 months.

Pros of this card: Firstly, this credit card offers complimentary Silver status in Hilton Honors. If card members spend more than $20,000 in a calendar year. The status will also upgrade to Gold Tier status.

Card members earn 7x points on eligible purchases in the Hilton hotels and resorts portfolio. They also earn 5x points on dining, takeouts, or delivery in US restaurants. Further, customers also earn 5x points on Groceries at the US supermarket. Cardmembers earn 5x points for gas at US gas stations. For the rest of the eligible purchases, they will earn 3x points.

Further, American Express also provides other offers for their card users. These include the Global Assist Hotline to offer assistance in case of an emergency. Car Rental Loss and Damage Insurance Protection for rental cars. Complimentary membership to ShopRunner with free 2-day shipping.

Hilton Honors American Express Surpass Card

Fees: This credit card charges $95 in annual fees but no charges on foreign transactions.

Rewards: Card members also earn 150,000 Hilton Honors Bonus Points. They have to spend $3,000 in purchases on this credit card within the first 6 months of the credit card membership.

Pros and Cons of this card: Firstly, this credit card offers complimentary Gold status in Hilton Honors. They can also get a free upgrade to the Diamond tier on spending $40,000 in a year. Further, members can earn a free night of spending $15,000 in a year.

Card members earn 12x points on eligible purchases in the Hilton hotels. They also earn 6x points on dining and takeout at US restaurants. In addition, they earn 6x points on gas at US gas stations. They also earn 6x points for groceries at US supermarkets. For the rest of the eligible purchases, they earn 3x points.